Insight Focus

A dry start to the monsoon in Maharashtra could reinforce the government’s hesitance to permit exports. The government may need to increase ethanol prices to encourage mills to divert more sucrose to ethanol.

A Dry Start to the Monsoon in Maharashtra

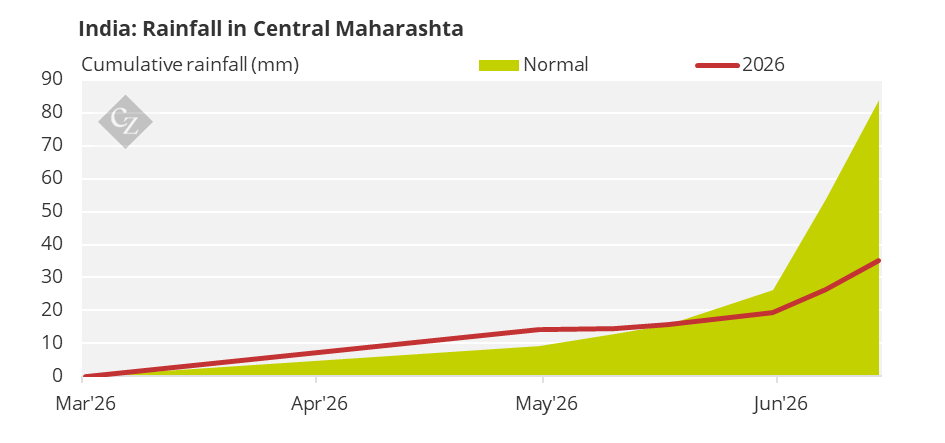

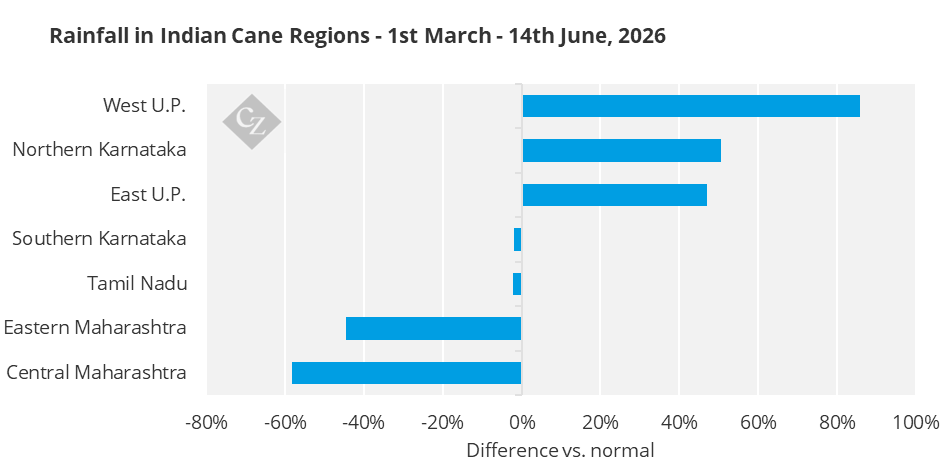

We’re two weeks into India’s monsoon season (which officially begins on June 1). Rainfall in Maharashtra has so far been around half of normal levels. This is in line with the Indian Meteorological Department’s forecast of a below average monsoon this year. It’s also in line with what we’d expect in an El Niño year.

India is a large country and, interestingly, conditions have varied between regions. Mostly notably, Northern Karnataka, which neighbours Maharashtra and which is also a major sugar producing region, has had better than normal rainfall far.

Similarly, in northern India, pre-monsoon showers have supported cumulative rainfall in Uttar Pradesh.

Although it’s still early in the monsoon season, developments in Maharashtra do reinforce our view that the government will be hesitant to permit sugar exports in 2026/27. It’s already suspended exports for the rest of 2025/26 (i.e. until September 30, 2026).

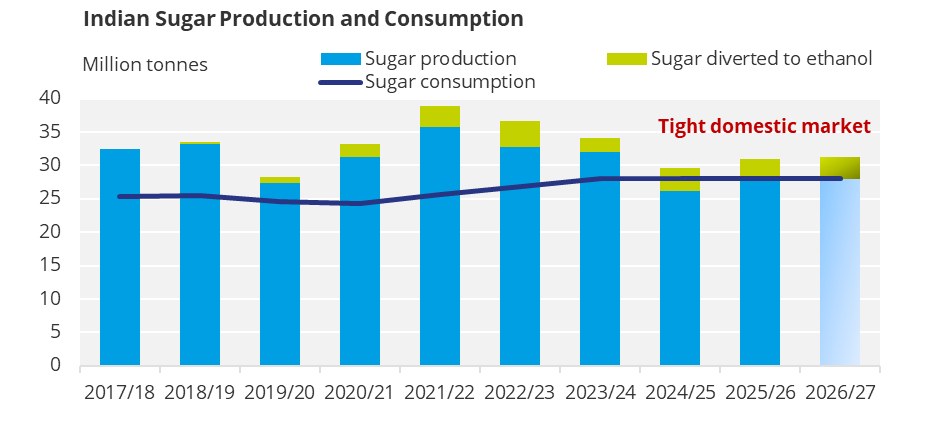

Following two years of a tight market, we don’t think the government would want to risk sugar shortages by permitting exports. Aside from controlling food inflation, the government will want to prioritise ethanol production over sugar exports. India is seriously looking at ways to better utilise its substantial ethanol production capacity to reduce dependence on imported energy.

The measures include increasing ethanol’s blend in petrol, introducing flex-fuel vehicles, using ethanol in cooking stoves and exploring blending ethanol in diesel. Earlier this month’s India’s first flexi-fuel car was sold, and the government and industry are looking at ways to scale consumer adoption. This includes establishing competitive pricing and taxation, updating vehicles’ technical capacity to use higher blends, and investing in pump infrastructure.

Exports Would be Attractive if they were Permitted

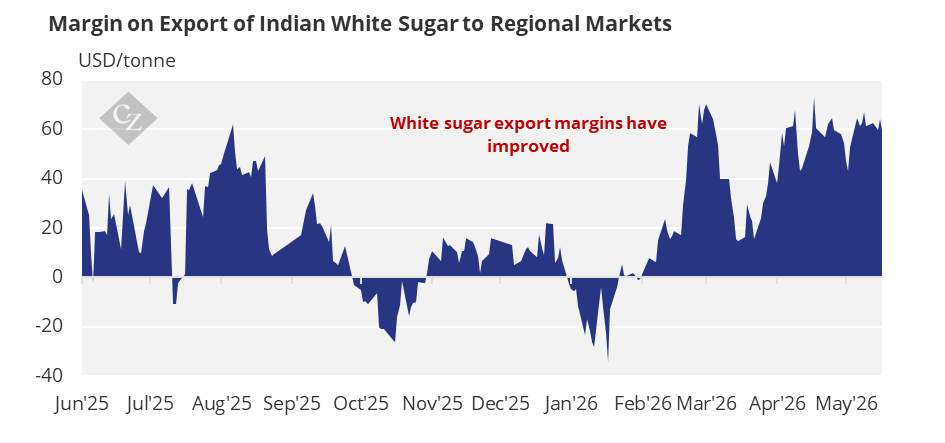

Positive margins on white sugar exports to regional markets (East Africa and South Asia) in theory could mean that shipments could pick up if the export ban isn’t extended into 2026/27.

Such a scenario could arise if the recent opening of the Strait of Hormuz alleviated energy costs and eased pressure to increase ethanol production. As we discuss below, cane mills may need higher ethanol prices to divert more sugar to ethanol, and the government could well be less willing to raise them if oil prices fall.

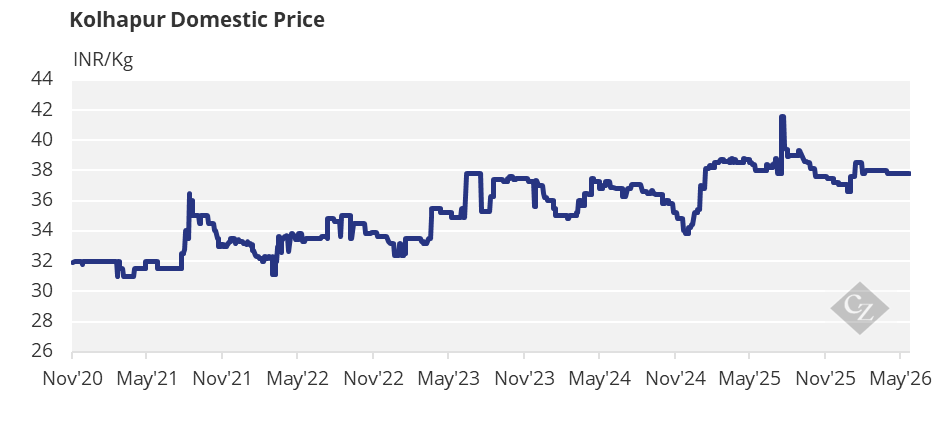

Domestic prices have stayed firm since February at around INR 38,000/tonne (ex-mill, Maharashtra). Positive export margins instead primarily reflect a weaker Indian Rupee, which has depreciated around 5% against the US Dollar since March.

A strong white premium has also boosted the theoretical margins. However, if India did return to the export market, white premiums could ease.

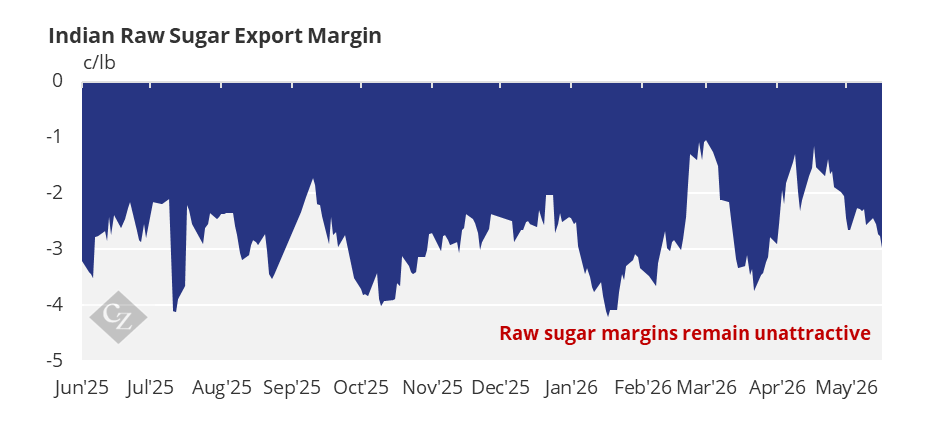

Meanwhile, the No.11 price required to make Indian raw sugar exports is over 16.5c/lb. As mills would lose over 2.5 c/lb on raw sugar exports, we don’t see India exporting raw sugar in the foreseeable future.

Ethanol Prices may Need to be Higher to Increase Sucrose Diverted to Ethanol

The attractiveness of ethanol vs. sugar remains an important issue to follow for 2026/27 given both the government and the sugar industry’s rapidly deepening focus on expanding ethanol production.

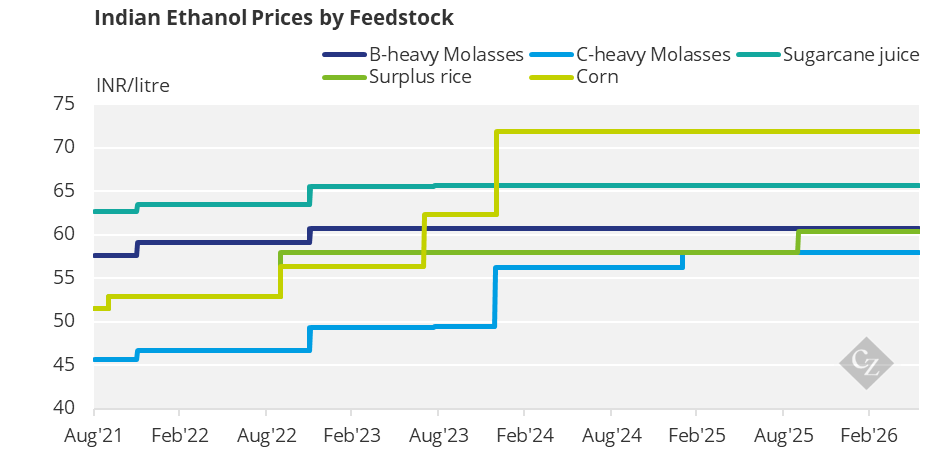

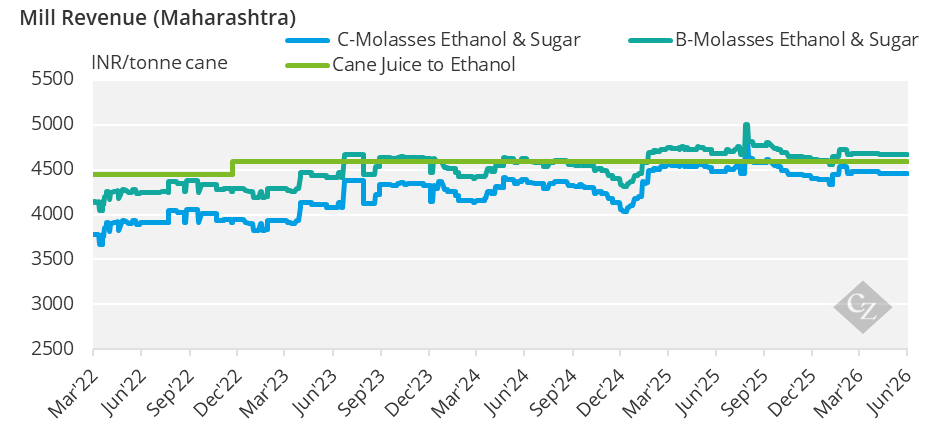

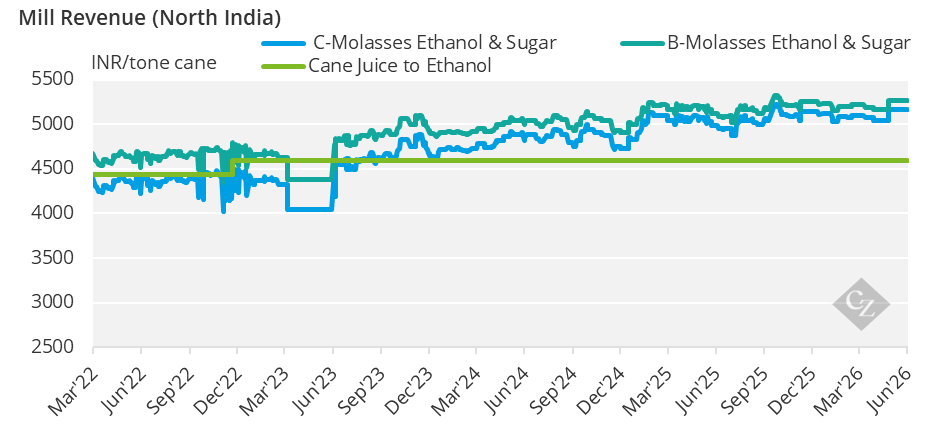

However, the government hasn’t increased the price of ethanol made from cane juice and B-heavy molasses for almost four years. As Indian sugar prices have been edging up during that time, mills have had little incentive to divert more sugar to ethanol.

This is particularly so in Northern India, where sugar prices are higher than in Maharashtra. The price of ethanol relative to sugar may have to rise much more than today’s levels to encourage more diversion to ethanol in this part of the country.

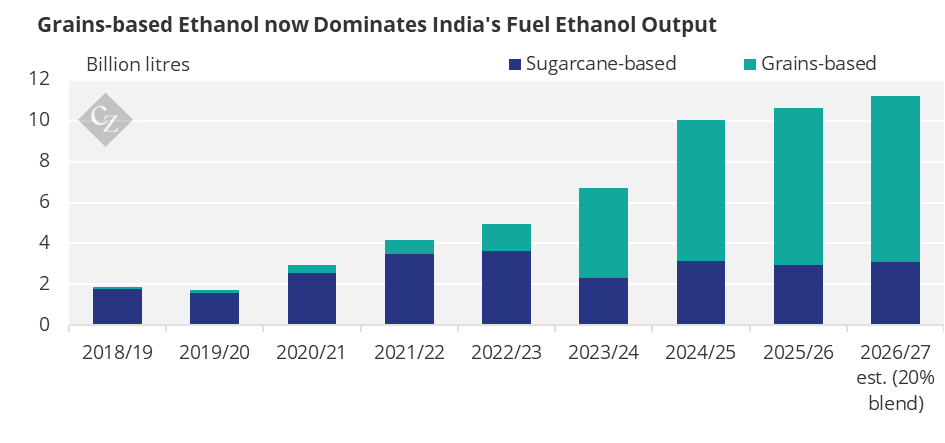

We can see the impact of unattractive ethanol prices on production. Ethanol produced from sugarcane has been stuck at 3-4 billion litres for five years, despite there being capacity to make 9 billion litres. The grains sector has instead been supplying the growth in Indian fuel ethanol demand.

Appendix

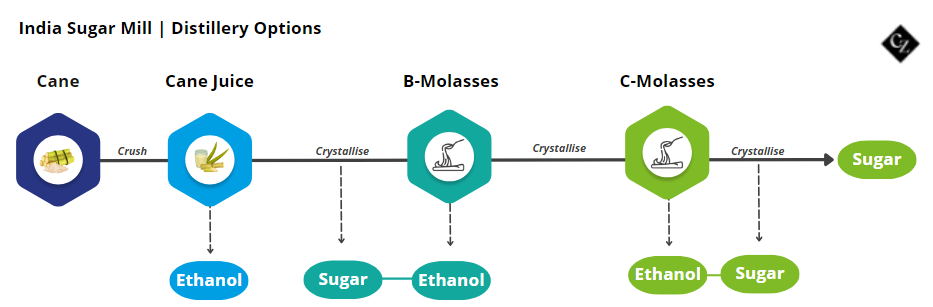

Our analysis considers the returns that mills earn from producing ethanol at the expense of sugar. Many mills/distilleries have a choice over which feedstocks they use to make sugar or ethanol based on the relative prices of ethanol paid by the oil marketing companies (OMCs), which is summarised below:

Proportion of Sugar to Ethanol: